Fair treatment of vulnerable customers

20 Apr 2020

The fair treatment of vulnerable customers is core to the FCA’s stated mission “to serve the public interest through the objectives given to it by Parliament” and this goal has been the subject of the regulator’s attention increasingly over the past years. The FCA has set out as a target outcome in its Business Plan 2020/21[1] the fair treatment of vulnerable customers while noting that technology and data can lead to the benefit or the detriment of the consumer. The regulator’s principles-based approach leaves some grey areas where the firms need to apply judgement on how to approach the broadness and complexity of the issue.

Vulnerability can affect anyone and can take many forms. Most of us will be at risk at some point in our lives and an improper interaction with financial services can lead to stress, indebtedness, and take up of unsuitable products. The life insurance industry can service vulnerable customers by providing support and peace of mind to improve their lives and wellbeing. Extreme events like Covid-19 can trigger economic shocks with detrimental impact to vulnerable customers with high accumulated levels of debt, pre-existing conditions and unstable income.

A vulnerable consumer is someone who, due to their personal circumstances, is especially susceptible to detriment, particularly when a firm is not acting with appropriate levels of care.

- FCA

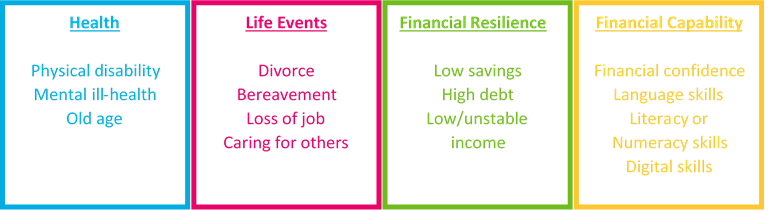

Drivers of vulnerability

2017 FCA Financial lives survey results[2]

One of the primary sources of information which informs the FCA’s perspective on vulnerable customers is the financial life survey which found that half of the UK adult population shows characteristics of potential vulnerability.

“A potentially vulnerable customer is someone who shows characteristics related to low financial resilience, a recent experience such as divorce or bereavement, low financial capability, or a health issue that affects day-to-day activities a lot.” – Financial lives survey

Levels of vulnerability varied only slightly by different age groups but older groups (75s and over) showed a higher proportion of vulnerability characteristics. An important subgroup of vulnerability as shown above is financial resilience. The FCA defines someone as being in financial difficulty if they have missed credit commitments over the last three months. They are said to be ‘surviving’ if they :

- Find it hard to keep up with bills

- Have no investable assets

- Would find it hard to keep up with an increase in mortgage/rent

- Have no savings to cover one month of no income

Other parts of society struggle in their interactions with insurers and recent research[3] highlighted in the FCA’s paper GC19/03, shows that 3 million people in the UK with disabilities have been turned down for insurance or charged extra. Furthermore, only 1 in 3 people with severe mental health problems have home insurance or a savings account and 1 in 4 people with cancer of those surveyed feel that the financial services industry unfairly discriminates against them. The worrying conclusion is that only 40% of UK adults are confident in the UK financial service industry, with just 31% feeling that financial firms are honest and transparent.

Out of the 1407 respondents who had a life insurance policy, 33% were identified as potentially vulnerable (according to the 4 drivers), 1% in financial difficulty and 27% surviving.

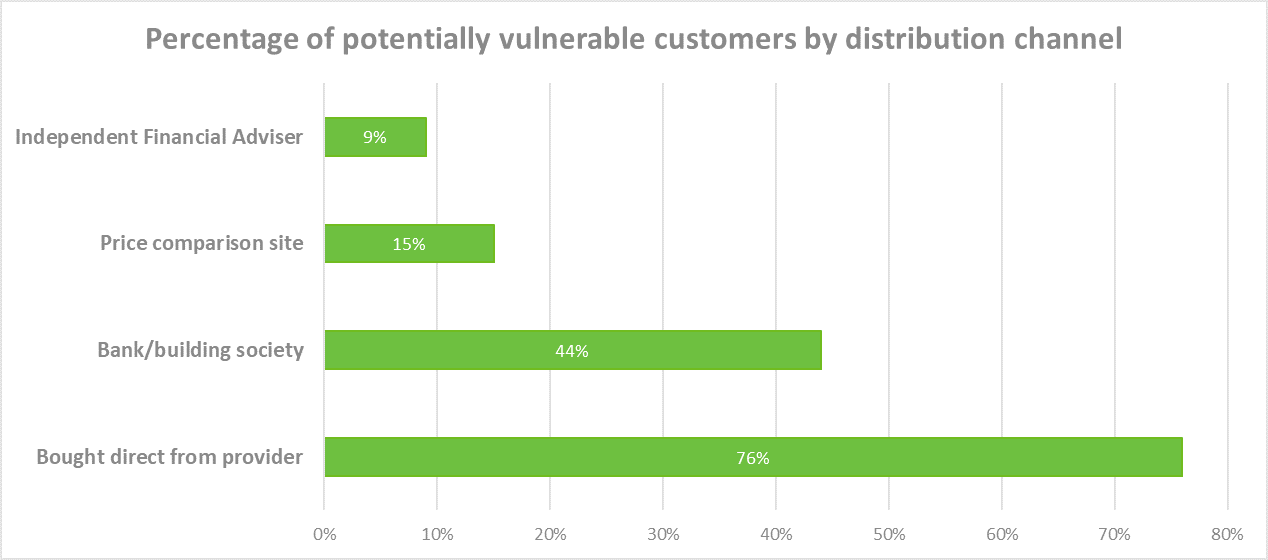

Another critical area to consider is the way in which financial products are purchased and the FCA survey/research highlighted some relevant statistics on this:

- 76% of people who bought directly from the provider were identified as potentially vulnerable

- 9% of people who bought through IFA’s are potentially vulnerable

- Only 15% of people who bought through comparison websites were identified as potentially vulnerable

(Click image to enlarge)

- Most vulnerable customers have not read the documentation carefully when taking out or renewing their policy, only 13% of vulnerable customers read the document, 69% looked through it briefly

- 56% of potentially vulnerable customers have either not reviewed their policy since inception or more than 5 years ago compared with 43% of not potentially vulnerable customers

We have highlighted the ways that insures could incorporate the findings from this research into their product development processes in the next section.

Considerations for insurers

(Click image to enlarge)

Better target market understanding along with their vulnerabilities can improve risk mitigation in pricing, product design and distribution. A sympathetic approach will benefit insurers in the long term and improve the public’s confidence in insurers. Embedding the fair treatment of vulnerable customers into the firm’s strategy will help their image, improve shareholder confidence and prove as evidence to the industry’s commitment to social responsibility. Opportunities for new markets exist and insures must realise the potential monetary and ethical benefits of serving financially under-served groups.

We are intending to publish more research on this area (see here for previous thoughts on general conduct risk approaches). If this is an area you would like to discuss please get in touch.

How Hymans Robertson can support you

Hymans Robertson has a wealth of experience in product design, regulation and conduct risk. We can assist you in reviewing the effectiveness of your existing policies for identifying and treating vulnerable customers.

0 comments on this post