Press release

Three quarters of DC members want automatic pension payments at retirement

Kathryn Fleming

Partner

Three quarters (75%) of DC pension savers aged 55 or over would find it helpful for their DC savings to start paying them an income automatically when they reached the point of retirement, research by Hymans Robertson has found. The research has been released today in the firm’s paper Designing decumulation defaults – remember the member. The paper argues the need for member-centric default decumulation design, something that can be a safety net for any member that doesn’t actively engage and make their own choices about their retirement income. It outlines the essential principles that providers should consider in scheme design. The leading pensions and financial services consultancy claims that too many members are at risk of poor outcomes through lost opportunities, expensive mistakes and fundamental confusion. Letting this continue is simply not acceptable and default decumulation will be essential.

The research for the paper also found that opt-out, employer review safeguards and timing around State Pension Age or earlier are high on savers’ wishes.

Commenting on the research findings, Kathryn Fleming, Head of DC At-Retirement Services, Hymans Robertson, said:

“The need for DC pension pots to deliver a sustainable income in retirement is ultimately the exam question the industry is trying to answer. There’s an ambition to get as many people as possible to engage with their retirement savings, but there will always be a significant number of people who won’t engage. It’s therefore essential that there’s a safety net in place for these individuals to give them the best chance of having good retirement outcomes.

“Members’ income sources for retirement are likely to be determined by more than just their DC savings, but it will be challenging to collate a picture of this across a scheme membership. It is also notable that as DC wealth increases, so too does the likelihood of an individual taking financial advice. In addition, there is significant evidence that small pots are simply cashed in. Any design is therefore likely to need flexibility to suit different segments of members.

“Pension schemes will also be starting from different positions, with different regulatory requirements and different membership profiles. The decision makers will also have different risk appetites, strategic objectives, commercial synergies, so differing solutions will evolve.”

The paper outlines a set of principles for providers to consider. These considerations include deciding priorities around strategic objectives and member needs, identifying risks, and understanding how the solutions fit with member behaviour once in retirement. The first principle which solution designers should follow is to identify what data they are using, what assumptions are made and how they may change over time. Secondly, they should know their members and what member needs their solution is aiming to meet, now and in the future. Thirdly, they should set their default design objectives and be clear on what a good member outcome will look like. Lastly, they should apply a risk lens and conduct scenario analysis and member testing.

Commenting on the developments that are needed, Kathryn continues:

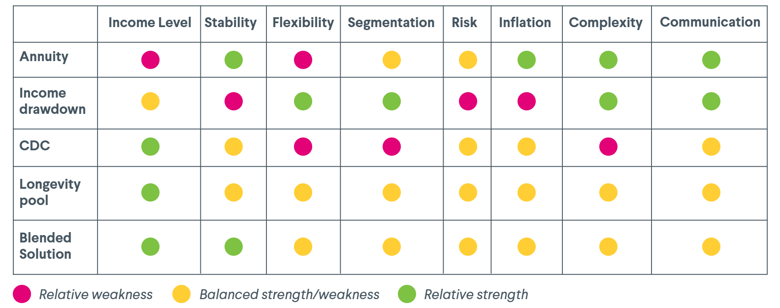

“As with most things in pensions, there’s not a perfect answer. But there are a number of options that are already available or are being explored by the industry that may feature in default decumulation solutions. These include annuity, income drawdown, and CDC, as well as longevity pooling and blended solutions.

“We would encourage providers to really seek to understand their average member’s needs now and in the future. People are complex and the data being relied upon to build a picture of an average member is incomplete. What members want or need from their DC retirement savings is exceptionally personal and varied, therefore the approach taken to designing something for an average member is going to require a lot of careful consideration. Finally, these solutions cannot be set and forget. In the absence of any upfront decision from a member, there needs to be consideration given to delayed engagement.”

The research can be read in the paper Designing decumulation defaults – remember the member here.